Contact

Contact Hoe winkelen bij ons werkt

Hoe winkelen bij ons werktBezorging

Winkelgids

Engels

Engels

349 b

349 b

Retourneren binnen 30 dagen

Klanten kochten ook

/

/

Gebonden (paperback)

Gebonden (paperback)

20.25

€

20.25

€

/

Gebonden (paperback)

28.35

€

/

Gebonden (paperback)

28.35

€

/

Gebonden (paperback)

29.16

€

/

Gebonden (paperback)

29.16

€

/

Gebonden (harde band)

66.43

€

/

Gebonden (harde band)

66.43

€

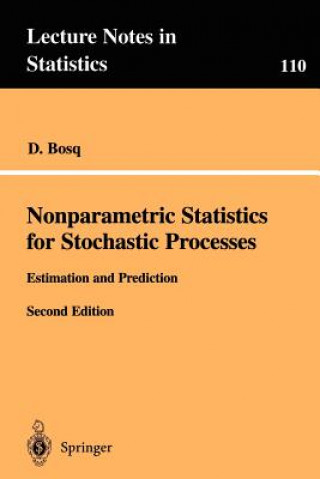

This book is devoted to the theory and applications of nonparametic functional estimation and prediction. Chapter 1 provides an overview of inequalities and limit theorems for strong mixing processes. Density and regression estimation in discrete time are studied in Chapter 2 and 3. The special rates of convergence which appear in continuous time are presented in Chapters 4 and 5. This second edition is extensively revised and it contains two new chapters. Chapter 6 discusses the surprising local time density estimator. Chapter 7 gives a detailed account of implementation of nonparametric method and practical examples in economics, finance and physics. Comarison with ARMA and ARCH methods shows the efficiency of nonparametric forecasting. The prerequisite is a knowledge of classical probability theory and statistics.

Informatie over het boek

Engels

Geef dit boek vandaag nog cadeau

Dat gaat heel eenvoudig

1 Voeg het boek toe aan je winkelwagentje en selecteer Als cadeau bezorgen 2 Je krijgt van ons per omgaand een voucher 3 Het boek wordt bezorgd op het adres van de ontvangerDit vind je misschien ook interessant

/

Gebonden (harde band)

25.11

€

/

Gebonden (harde band)

25.11

€

/

Gebonden (paperback)

26.02

€

/

Gebonden (paperback)

26.02

€

/

Gebonden (paperback)

33.31

€

/

Gebonden (paperback)

33.31

€

/

Gebonden (harde band)

240.54

€

/

Gebonden (harde band)

240.54

€

Hoi! Ik ben Libroamiko, je boekadviseur.

Hoe kan ik je helpen?